The Rise of Emerging Managers in Numbers

This is the second article in a series of posts on investments in young venture funds raised and run by emerging fund managers.

Saint Clair · Soft Due Diligence | July 2023

The first article in this series examined the qualitative case for investing in young venture funds. The case is real; what remains to settle is the magnitude of the rewards and the calibration of the risks.

This article gathers the quantitative insights we have collected in our research. The collection makes no claim to be exhaustive, and some of the data is beginning to look its age, but venture capital takes a long view and the underlying trend is discernible.

Who is an Emerging Fund Manager?

The definition of an Emerging Fund Manager varies across sources. Parameters are generally some combination of years of activity, number of funds raised, and fund size.

Pitchbook sets the bar at fewer than four funds raised. Other working definitions reach for vaguer criteria, such as “newly formed” or “relatively small”, leaving the spectrum open.

The difference in available track-record between a VC raising Fund I and one already benefitting from the experience of two or three prior funds is obvious. The harder case is the experienced spin-off GP from a mature platform raising his first solo fund alongside a relatively recent venture capitalist raising Fund II or III. The numerical bar tends to flatten the substance of either.

In our reading, the answer comes down to context. “Emerging” is a working decision criterion held by the people the manager interacts with, in particular prospective LPs. The label is what each LP makes of it, calibrated to that LP’s own portfolio constraints and ambitions.

An LP works with a focussed investment approach and a working risk-mitigation strategy. Part of that is a set of criteria that draws boundaries between funds the allocation is open to and funds it is closed to. The criteria above will (or should) appear in the set, calibrated to the individual portfolio’s requirements and objectives.

Our own working definition is entrepreneurial rather than numerical. We consider Emerging fund managers those whose activity includes an element of exploration — a working quest to push boundaries. The boundaries may be the manager’s own (the venture capitalist starting out in the industry) or the industry’s (an investment thesis with a characteristic angle in sector focus, geography, or demographic).

The other “Emerging”

A second sense of “Emerging” runs through the literature: emergence by origin or diversity.

The venture capital industry has long been dominated by a homogeneous demographic. To oversimplify intentionally, by “white western males” from broadly similar cultural and academic backgrounds.

The side effect runs through similarity bias in venture financing. In their academic research, Franke et al. found that VCs assess founders with similar social and educational backgrounds more favourably [1]. Murnieks et al. produced converging evidence: VC fund managers prefer founders who think like themselves [2].

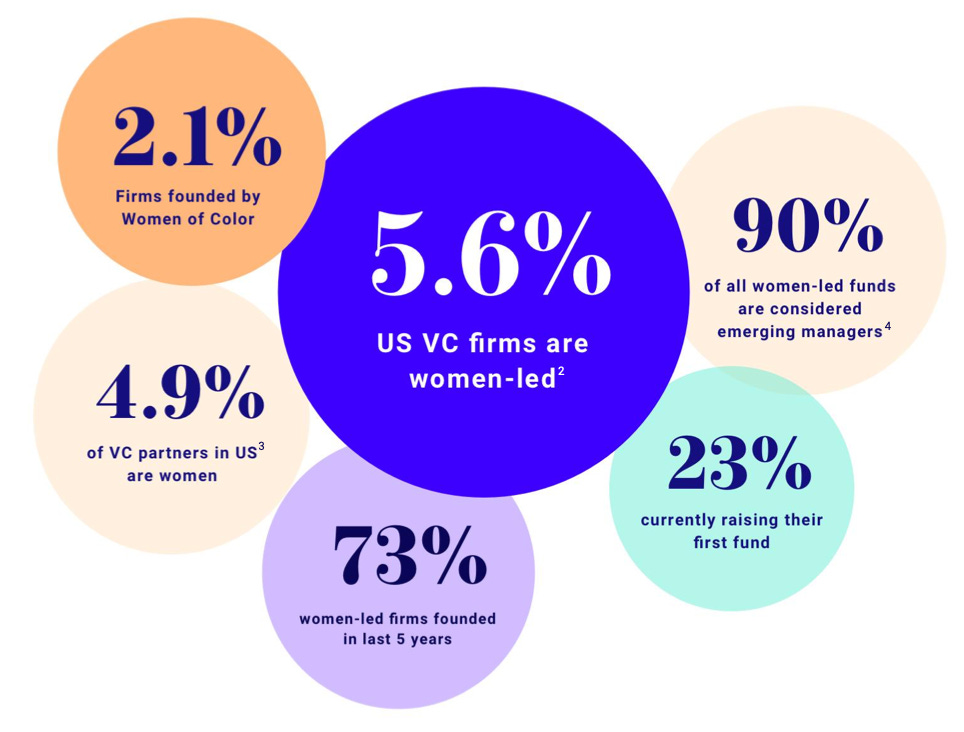

Female-led venture capital funds give the sharpest example. According to Pioneerspost [3], 90 per cent of female-managed funds had to be considered “Emerging” in 2021, on the criterion of managing their first or second fund at less than USD 100 million (see also the underlying study Women in VC [4]).

(Source Study “Women in VC”)

Beyond venture capital, the same article cites a study finding that only 1.4 per cent of US-based financial assets are managed by diverse-owned firms [5].

(Source: KNIGHT DIVERSITY OF ASSET MANAGERS RESEARCH SERIES: INDUSTRY)

Emerging Fund Performance

The performance picture, read against the structural framing above, gives the LP a positive case for Emerging Managers.

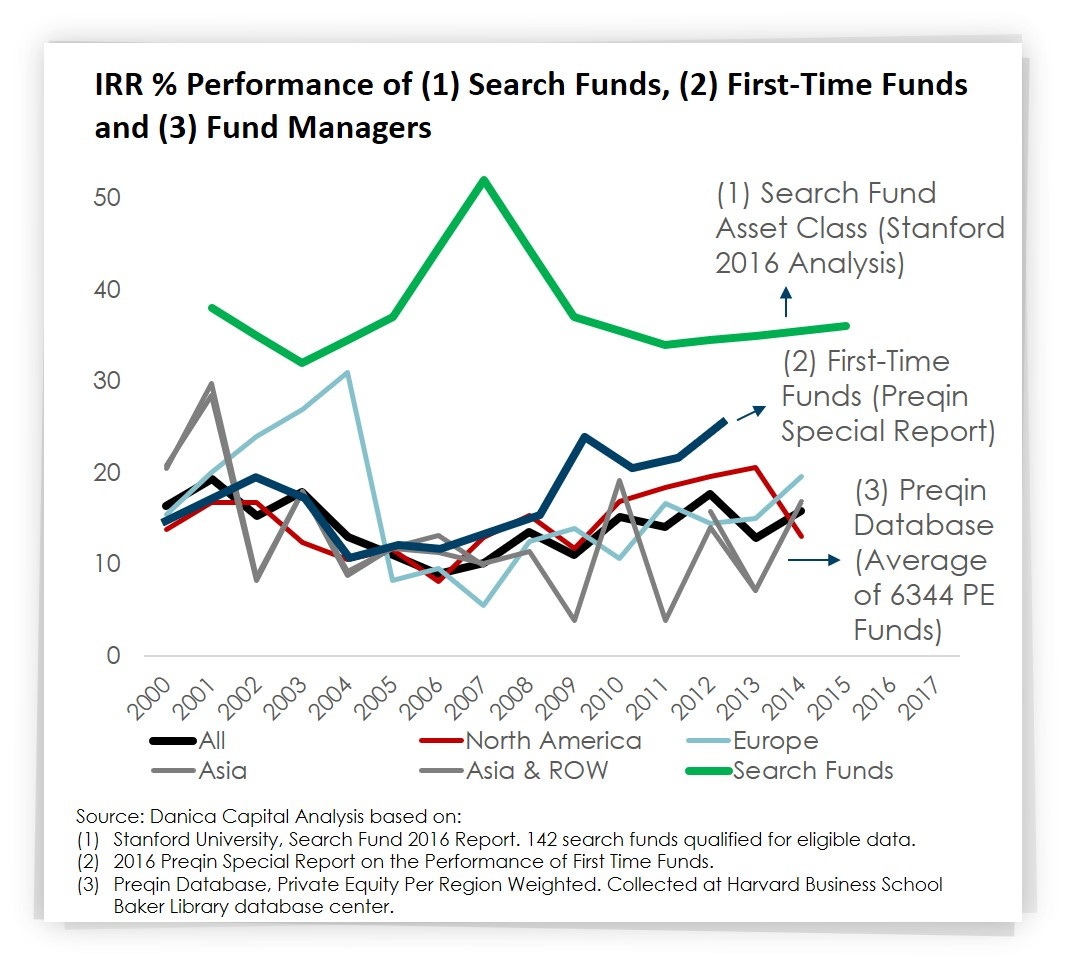

Pitchbook’s Q1 2021 Benchmarks Report finds that First Time Funds (FTF) significantly outperform “higher-numbered” funds while presenting a lower downside risk [6].

(Source: PitchBook, 2021)

The pattern appears consistent. A 2016 Preqin report states that "first-time funds have outperformed funds of established managers in every year except one (2004) over the past thirteen years" [7]. The data is seven years old at the time of writing, but venture capital operates on a long horizon where the underlying internal dynamics tend to hold.

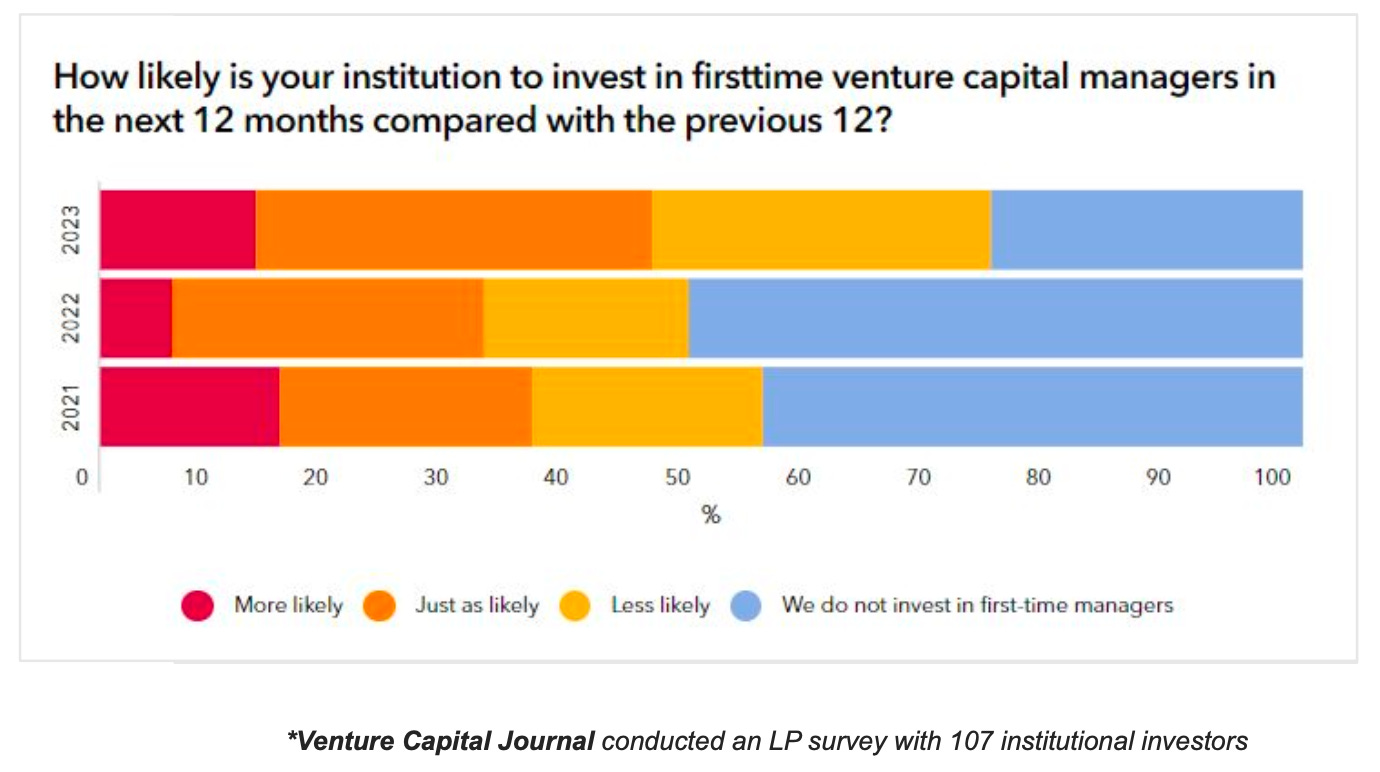

An updated edition of the Preqin study, capturing the macroeconomic shifts since, would be welcome reading. A 2023 study by Vauban [8] cites a Venture Capital Journal survey on LP willingness to invest in first-time managers.

The 2023 picture is mixed. More LPs say it is “less likely” they will invest in first-time managers; fewer LPs exclude it completely; and the combined proportion responding “more likely” or “just as likely” is larger than in previous years.

The asset-allocation dynamics confirm the cooling. Axios reports that 62 per cent of capital has gone to 6 per cent of funds, and that in Q3 alone, 86.7 per cent of the money was committed to just 66 funds [9].

The shifts in global economics over the past twelve to twenty-four months, and the rise of the risk-free rate in particular, have left venture capital in choppier waters. A future article in this series will examine the particular challenges of being an Emerging Manager under the present conditions.

The Contribution of Emerging Managers

Emerging Managers’ contribution to the industry as a whole is substantive.

According to Cambridge Associates [10], Emerging Managers account for 72 per cent of the top-returning firms between 2004 and 2016, while receiving a smaller share of allocated capital than the more mature firms.

The same source consistently places first-time and emerging funds among the top ten performers across that period. The Vauban study cited above ranks them among the top five performers for vintages from 2004 to 2020.

On deal value created, Axios — drawing on Pitchbook data — confirms that emerging venture capital firms contribute substantially to industry value: consistently at least 25 per cent over the ten years to 2022, and approaching 50 per cent in the peak year of 2017.

Emerging Manager’s future?

The statistical case for investing in Emerging Managers holds, with the usual caveat that source selection carries biases. The reading is consistent with a wider view: Emerging Managers have a meaningful role to play in the risk-reward calculus of venture capital.

Becoming an Emerging Manager and earning credibility as a target for institutional allocation is hard work. The data, however, supplies a counterweight to the assumption that only the track record and experience of mature VC firms can promise value for LPs.

LPs may want to read Emerging Managers more favourably for the outsize returns they appear to generate. In current conditions, where allocation to VC funds is being penalised by more compelling alternatives and a low risk-free rate, an emerging fund is worth a closer look.

Emerging Managers graduate. The working goal is to graduate out of the category and build a successful track record. For LPs, building a portfolio of Emerging Managers is also building a pipeline of future, and one day access-restricted, high-performing VC funds.

As Rainer Braun, Professor of Entrepreneurial Finance at my alma mater TU Munich and co-founder of the venture fund-of-funds Equation, has put it: the successful unicorn hunters are the ones that invested at seed stage.

The next article in the series turns to the criteria and best practices LPs use to evaluate emerging fund managers, and the role of Soft Due Diligence in the process.

References

[1] Franke, N., Gruber, M., Harhoff, D., & Henkel, J. (2006). What you are is what you like — similarity biases in venture capitalists’ evaluations of start-up teams. Journal of Business Venturing, 21(6), 802–826.

[2] Murnieks, C. Y., Haynie, J. M., Wiltbank, R. E., & Harting, T. (2011). ‘I like how you think’: similarity as an interaction bias in the investor–entrepreneur dyad. Journal of Management Studies, 48(7), 1533–1561. https://doi.org/10.1111/j.1467-6486.2010.00992.x

[3] Pioneerspost (2023). Emerging and diverse fund managers outperform — here are five reasons why. https://www.pioneerspost.com/news-views/20230125/opinion-emerging-and-diverse-fund-managers-outperform-here-are-five-reasons-why

[4] Women in VC (2021). The Untapped Potential of Women-Led Funds. https://assets.ctfassets.net/jh572x5wd4r0/7qRourAWPj0U9R7MN5nWgy/711a6d8344bcd4fbe0f1a6dcf766a3c0/WVC_Report_-_The_Untapped_Potential_of_Women-Led_Funds.pdf

[5] Knight Foundation (2021). Knight Diversity of Asset Managers Research Series: Industry. https://knightfoundation.org/wp-content/uploads/2021/12/KDAM_Industry_2021.pdf

[6] Pitchbook (2021). Q1 2021 Benchmarks Webinar Deck. https://files.pitchbook.com/website/files/pdf/Q1_2021_Benchmarks_Webinar_Deck.pdf

[7] Preqin (November 2016). Special Report: Making the Case for First-Time Funds. http://docs.preqin.com/reports/Preqin-Special-Report-Making-the-Case-for-First-Time-Funds-November-2016.pdf

[8] Vauban (2023). LP for Emerging Fund Managers. https://vauban.io/post/lp-for-emerging-fund-managers

[9] Axios Pro Rata (2022). https://www.axios.com/newsletters/axios-pro-rata-083a5f20-d970-4827-8870-ddd46338e29c.html

[10] Cambridge Associates. Venture Capital Positively Disrupts Intergenerational Investing. https://www.cambridgeassociates.com/insight/venture-capital-positively-disrupts-intergenerational-investing/

Sources: References as numbered citations above. Originally published 17 July 2023 on softduediligence.com. Revised under Saint Clair editorial, 2026; the 2026 longitudinal update is published as a companion piece — Emerging Managers in Numbers, Three Years On.

Disclaimer: This article is for informational purposes only and does not constitute investment or business advice. All decisions should be made based on independent research and consultation with qualified advisors.

About Saint Clair — Advisory & Capital: Saint Clair designs and builds cross-border capital infrastructure between Europe and Asia — proposing access where access is scarce, and creating structure where structure is absent. We guide Asian technology companies through European market entry, partnership development, and cross-border expansion. Since 2016.

Learn more: saintclair.sg | Contact: contact@saintclair.sg